Introduction: Policy Details That Affect Your Financial Security

When evaluating Disability Insurance, many focus on monthly benefits but overlook critical policy details. Coverage limits and waiting periods directly influence how well a policy protects income during disability.

Understanding these elements helps U.S. workers, professionals, and self-employed individuals select the right policy, avoid coverage gaps, and ensure long-term financial stability.

This article explains disability insurance coverage limits and waiting periods, their impact on income protection, and practical strategies for choosing optimal coverage.

What Are Disability Insurance Coverage Limits?

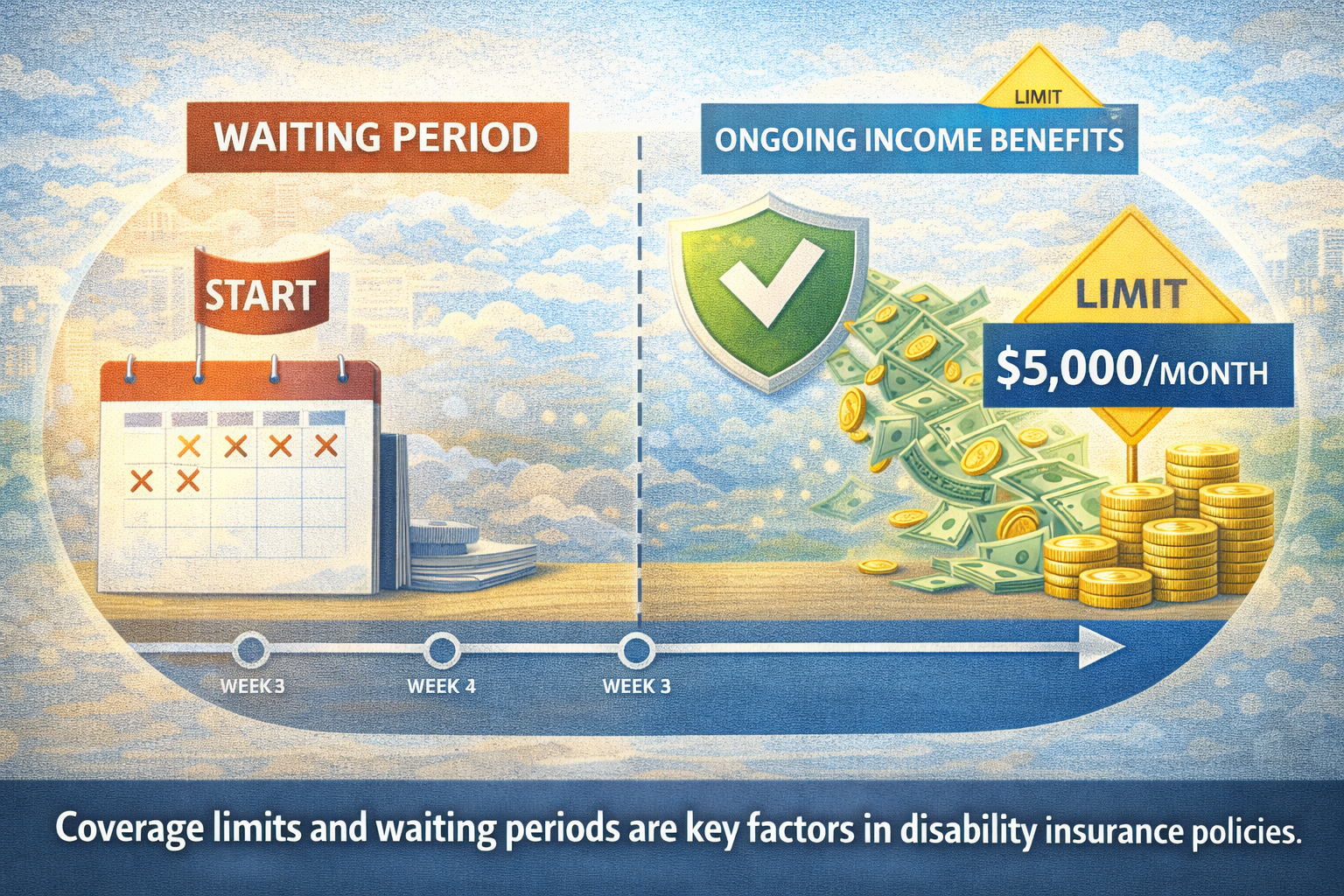

Coverage limits define the maximum benefits a policy will pay. They determine:

-

The maximum monthly or annual income replacement

-

Total lifetime or benefit-period payout

-

Limits on specific types of disabilities or conditions

There are several common types of limits:

-

Monthly Benefit Maximums

-

Caps the monthly income replacement

-

Typical range: $5,000–$15,000 per month for employer plans

-

High earners often require supplemental individual coverage

-

-

Benefit Period Limits

-

Defines the length of time benefits are paid

-

Common periods: 2 years, 5 years, until age 65, or lifetime

-

Longer benefit periods increase premium costs

-

-

Policy-Specific Caps

-

Some policies impose sub-limits for mental health or chronic conditions

-

Exclusions or maximum payouts may vary by insurer

-

Understanding these limits ensures that your policy adequately protects your income without leaving gaps.

How Waiting Periods Affect Disability Insurance

A waiting period, also known as the elimination period, is the time between the onset of a disability and when benefits begin.

Key Features:

-

Typically ranges from 14 days to 180 days

-

Short-term Disability Insurance often has waiting periods of 0–14 days

-

Long-term Disability Insurance usually has waiting periods of 90–180 days

-

Waiting periods affect monthly premiums—longer waiting periods generally reduce premiums

During the waiting period, policyholders must rely on:

-

Emergency savings

-

Sick leave or PTO

-

Short-term coverage, if available

Choosing an appropriate waiting period balances affordability with income protection needs.

Interaction Between Coverage Limits and Waiting Periods

Both coverage limits and waiting periods work together to define actual income protection:

-

High monthly limits may be useless if waiting periods are long and savings are insufficient

-

Short waiting periods with low coverage may provide inadequate income replacement for high earners

-

Understanding both factors is critical to designing a comprehensive strategy

Examples of Coverage Limit Scenarios

Scenario 1: Mid-Level Employee

-

Annual income: $80,000

-

Employer STD policy: 60% of income, $4,000/month cap, 14-day waiting period

-

LTD policy: 60% of income, $6,000/month cap, 90-day waiting period

In this case, income replacement may fall short during the waiting period without additional savings.

Scenario 2: High-Income Professional

-

Annual income: $250,000

-

Employer LTD cap: $15,000/month

-

Individual Disability Insurance supplements the cap

-

Waiting period: 90 days for LTD

-

COLA rider ensures benefit keeps pace with inflation

This demonstrates the importance of understanding both limits and waiting periods for high-earning professionals.

Choosing the Right Coverage Limits

To determine appropriate coverage limits:

-

Compare monthly income replacement with living expenses

-

Review benefit periods in relation to potential disability duration

-

Consider existing employer coverage and supplemental policies

-

Account for family and financial responsibilities

-

Factor in inflation and cost-of-living adjustments

Higher coverage limits increase premium costs but also improve financial security during long-term disabilities.

Selecting an Appropriate Waiting Period

Waiting periods should be chosen based on:

-

Size of emergency savings

-

Availability of sick leave or short-term coverage

-

Comfort with financial risk during the initial disability period

A balanced approach often combines:

-

Short waiting period for immediate protection (STD)

-

Longer waiting period for cost-efficient long-term coverage (LTD)

Common Policy Pitfalls

-

Ignoring monthly benefit caps

-

Overlooking exclusions for specific conditions

-

Selecting a waiting period too long for your savings level

-

Assuming employer coverage alone is sufficient

-

Not reviewing policies as income grows

Practical Planning Recommendations

-

Layer short-term and long-term coverage

-

Supplement employer plans with individual policies if income exceeds caps

-

Choose waiting periods aligned with personal savings and financial flexibility

-

Periodically review limits as income and expenses change

-

Include COLA or inflation protection for long-term planning

These strategies ensure maximum effectiveness of Disability Insurance policies.

Key Takeaways

-

Coverage limits determine the maximum benefits you can receive

-

Waiting periods delay income replacement and must align with financial resources

-

Both factors critically impact your ability to maintain financial stability during disability

-

High earners and self-employed professionals may require supplemental coverage

-

Periodic review of limits and waiting periods is essential for ongoing protection

Conclusion

Understanding disability insurance coverage limits and waiting periods is as important as understanding income replacement percentages. Without attention to these details, policies may leave significant gaps in protection, particularly for high-income earners or self-employed individuals.

By carefully evaluating limits, benefit periods, and waiting periods, U.S. workers can select a Disability Insurance policy that truly preserves income and ensures long-term financial security—even when disability strikes unexpectedly.

Leave a Reply